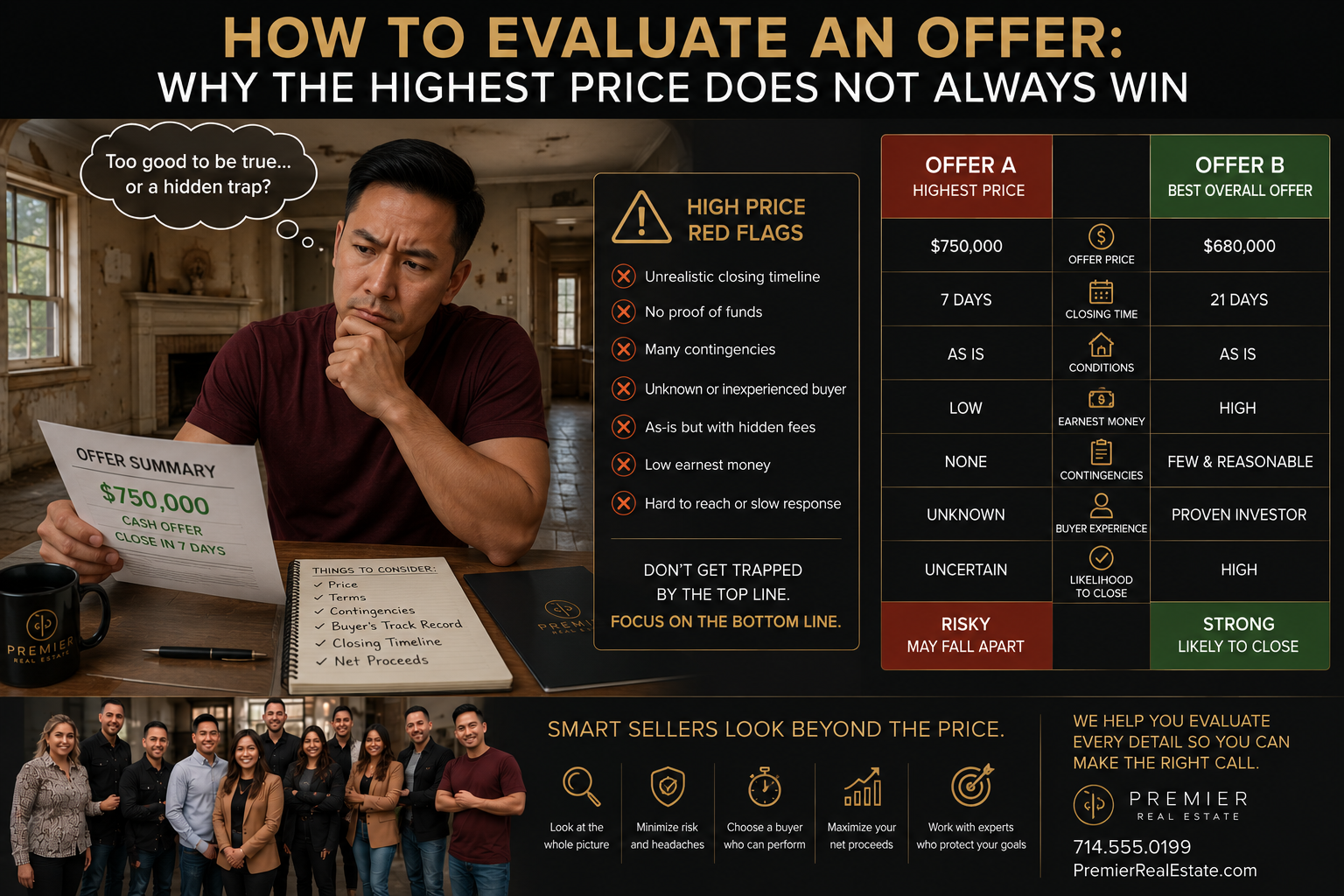

When the offers start coming in, almost every seller does the same thing. They look at the top number on each one and try to decide based on that. It is the natural place to start, but it is not the right place to stop. The strongest offer is rarely just the highest price. The strongest offer is the one most likely to actually close, on a timeline that works for you, with the fewest ways it can fall apart along the way. Picking the wrong offer based purely on price can cost you weeks of wasted time, a second relisting at a worse moment, and ultimately less money in your pocket than if you had chosen the slightly lower offer with the cleaner terms. Here is how to read an offer fully so you make the call that actually serves you.

The first thing to look at on any offer is how the buyer is paying. Cash offers are the gold standard for one simple reason. There is no lender involved who might pull back, no loan that might not get approved, and no appraisal that might come in low. A cash buyer who proves funds can typically close in two weeks or less, and there is almost no path for the deal to fall apart due to financing. Financed offers can absolutely still be strong, but you need to look at the specifics. There is a real difference between a pre-approval and a pre-qualification, and a lot of sellers do not realize it. A pre-qualification is a casual estimate from a lender based on what the buyer said about their finances. A pre-approval means the lender actually verified income, assets, and credit and committed in writing to lending a specific amount. Pre-approval is the only one that carries real weight. Loan type matters too. A conventional loan from a strong buyer is the most predictable. FHA and VA loans have stricter property and appraisal requirements that can slow or complicate closing. Jumbo loans require deeper underwriting. None of these are automatic disqualifiers, but each one shifts the risk profile of the offer.

The next thing to read carefully is contingencies. Contingencies are escape hatches that let the buyer back out of the deal without losing their deposit. The most common ones are inspection, appraisal, and financing. An inspection contingency lets the buyer walk if something they do not like turns up during inspection, or gives them grounds to renegotiate the price afterward. An appraisal contingency lets them back out or renegotiate if the home does not appraise for the contract price. A financing contingency lets them out if their loan falls through. Every contingency the buyer keeps in the contract is another way the deal can unravel before closing. Offers that waive or shorten these contingencies are stronger from a certainty standpoint, even at the same price. The honest tradeoff is that buyers writing more aggressive terms often expect a slightly lower price, because they are taking on more risk themselves. A clean offer at a slightly lower price is often a better deal than a higher offer loaded with contingencies, because the clean one is much more likely to actually close. The seller's question is not just "what is the price?" It is "what is the price after I weigh the risk of this deal falling apart?"

Earnest money is the deposit a buyer puts down when they go into contract, and it sits in escrow until closing. The size of that deposit tells you how serious the buyer is. A larger earnest money deposit, typically three percent of the purchase price or more in this market, signals real commitment, because the buyer stands to lose it if they back out without a valid contingency. A smaller deposit signals the opposite, that the buyer is keeping their downside risk small in case they change their mind. The closing timeline matters too. Some sellers need a fast close, sixty days down to thirty, while others need extra time to find a replacement home or coordinate with a job change. The right offer matches your timeline, not someone else's. Possession is another lever. Sometimes buyers offer a rent-back arrangement that lets you stay in the home for a period after closing, which can be valuable if you need a bridge between this sale and your next move. And seller concessions are a real line item too. A buyer asking for credits at closing is effectively asking for a price reduction in another form. Read those numbers fully before you compare offers head to head.

Here is one of the biggest hidden risks on a financed offer. The buyer's lender is going to send an appraiser out to the home to confirm the contract price matches the property's value. If the appraisal comes in below the agreed price, the lender will only loan against the lower number, and the buyer has to either come up with the difference in cash, renegotiate the price down, or walk away from the deal. In a normal market this is rarely a problem. In a hot market where homes are selling above asking, appraisal gaps happen all the time. Some buyers will protect against this by including an appraisal gap clause, where they commit in writing to covering some or all of the difference between the appraisal and the contract price out of their own pocket. That clause is a strong signal of buyer commitment and significantly reduces the risk to you as the seller. An offer with a meaningful appraisal gap built in can be worth more than a higher offer without one, depending on the situation.

Once you have all that information in front of you, the real decision is about weighing three things together. Price, certainty, and timeline. The highest price is meaningless if the deal does not close. A bulletproof offer at a slightly lower price often nets you more money than a fragile offer at a higher one, because you do not end up back on the market three weeks later with a stale listing and weaker offers waiting. Timeline matters too. An offer that closes fast might be worth a small price concession if your circumstances require it. An offer that lets you stay in the home for a month after closing might be worth more than one demanding immediate possession. The strongest offer is the one that best fits your goals across all three dimensions, not the one with the biggest headline number. Picking that offer is where good representation actually earns its keep.

When offers come in, every seller deserves a clear, honest breakdown of what each one really means. Not just the price, but the financing, the contingencies, the earnest money, the timeline, and the realistic odds of each deal closing on its terms. We sit down with sellers and walk through every offer line by line, side by side, so the choice is based on the full picture instead of just the top number. The goal is to help you pick the strongest offer for your situation, not just the biggest one. Reach out when offers start coming in, or even before, so we can make sure you choose well when the moment arrives.

Check out this article next